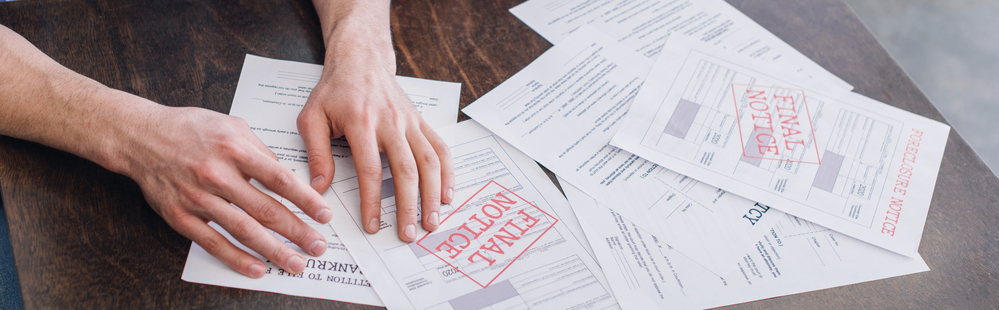

If you’re facing financial hardship or behind on mortgage payments, you might be wondering whether a short sale is an option. The idea to short sell a house can sound complicated, but it’s simply a way to avoid foreclosure and move forward with less damage to your credit.

In this guide, we’ll break it down in plain terms—no jargon, just helpful steps and honest pros and cons.

1. What Does It Mean to Short Sell a House?

To short sell a house means selling it for less than the amount you still owe on the mortgage. The lender agrees to accept the lower sale price to avoid the costly process of foreclosure.

For example, if you owe $200,000 on your mortgage but can only sell your home for $170,000, the lender may approve that sale to recover as much as possible. The remaining balance is either forgiven or collected later—depending on state laws and the lender’s policies.

2. When Is a Short Sale a Good Option?

A short sale is often the best path forward when you’re stuck in a financial bind and can no longer keep up with mortgage payments. Here are some common situations where it makes sense to short sell a house:

- You’re behind on your mortgage payments. If you’ve missed multiple payments and can’t catch up, a short sale can prevent foreclosure.

- Your home is worth less than you owe. This is often called being “underwater” on your mortgage, and it makes selling through traditional means difficult.

- You’re facing foreclosure. A short sale allows you to avoid the lengthy and damaging foreclosure process, which stays on your credit report for up to seven years.

- You’ve experienced a major life hardship. Events like job loss, divorce, death in the family, or unexpected medical bills can all qualify as valid reasons to request a short sale from your lender.

Short sales are not for everyone, but they are often viewed as a last-resort solution that helps homeowners exit a tough situation with less long-term damage. Unlike foreclosure, you maintain more control over the process and can start rebuilding your financial health sooner.

3. How the Short Sale Process Works

Here’s what the process generally looks like:

Step 1: Prove Financial Hardship

Your lender will require documentation showing why you can’t continue making payments—such as job loss, divorce, or medical emergencies.

Step 2: Get a Real Estate Agent or Cash Buyer

You’ll want someone experienced in short sales. Some sellers go through agents; others choose a cash buyer for faster results.

Step 3: List the Property or Secure a Buyer

Depending on your approach, you’ll either list the property or find a buyer who can make an offer your lender might accept.

Step 4: Submit Offer to the Lender

You’ll submit the purchase offer to the bank, along with a hardship letter and other documentation.

Step 5: Wait for Lender Approval

This part can take weeks or even months. The lender may counteroffer, approve the deal, or reject it.

Step 6: Close the Sale

Once approved, the sale goes through, and the home is transferred to the new buyer. Your credit will take a hit—but it’s often less severe than a foreclosure.

4. Pros and Cons of a Short Sale

✅ Pros:

- Avoids foreclosure and the emotional/legal weight that comes with it

- Less damage to credit than foreclosure

- May be able to buy again sooner than if you had gone through foreclosure

- You control the sale, not the bank

❌ Cons:

- Takes time—bank approval isn’t fast

- Not guaranteed—your lender can say no

- Your credit score will still drop

- Possible tax implications if the forgiven debt is treated as taxable income. The IRS provides guidelines on canceled debt and short sales, which can help you understand how this may affect your situation.

5. Short Sell House vs. Foreclosure: What’s the Difference?

When you’re behind on your mortgage and facing pressure, it’s easy to feel overwhelmed by your options. Two of the most common paths are foreclosure and short sale, but they are not the same—and they lead to very different outcomes.

Foreclosure:

Foreclosure is the legal process where your lender takes back the home after missed payments. It’s initiated by the bank, not the homeowner. Once the process begins, you may have little control. The property is typically auctioned off, and you may be evicted. A foreclosure stays on your credit report for up to seven years and significantly impacts your ability to borrow again in the near future.

Short Sale:

A short sale, by contrast, puts you in the driver’s seat. You work with your lender to sell the home for less than what you owe, but you have the opportunity to participate in the sale and potentially negotiate terms. The impact on your credit is still negative, but it’s usually less damaging than a foreclosure, and you may be eligible to buy another home sooner.

In states like Michigan, lenders may even prefer a short sale over foreclosure. It saves them time, legal fees, and the risk of ending up with an unsold property on their books.

By choosing to short sell, you also gain peace of mind knowing you took proactive steps to resolve the situation rather than letting it escalate.

6. Local Insight: Short Sales in West Michigan

In areas like Grand Rapids, Kentwood, Muskegon, Belding, Holland, and Wyoming, housing prices have seen ups and downs over the past few years. If you currently owe more than your home is worth, a short sale might be a practical solution to avoid foreclosure.

West Michigan has a mix of older homes, inherited properties, and homes with deferred maintenance that may not sell easily on the traditional market. Homeowners in these situations often find that a short sale or a direct cash offer helps them exit their mortgage faster with less financial damage.

At Hometown Development, we specialize in helping Michigan homeowners navigate tough real estate decisions. Our team understands the unique challenges of short sales and works directly with lenders to streamline the process.

Whether you’re based in Grand Rapids, Kentwood, Holland, Belding, or Muskegon, we’re familiar with your local market and can offer guidance tailored to your situation. We’ve seen firsthand how a short sale can provide relief and help homeowners regain control over their financial future.

If you’re exploring a short sale and want to understand your options, contact our team today.

7. Alternatives to a Short Sale

Before committing to a short sale, consider:

- Loan modification – renegotiate the terms of your mortgage

- Refinancing – may not be available if you’re already behind

- Renting the home out – only works if you can cover the mortgage

- Selling to a cash buyer – can sometimes offer a solution faster than a short sale process

Final Thoughts: Is a Short Sale Right for You?

If you’re underwater on your mortgage and need a way out, a short sale can offer relief—without the long-lasting impact of foreclosure.

It’s not always easy, but it is possible with the right help.

💬 Need Help Navigating a Short Sale?

If you’re in Grand Rapids, Kentwood, Holland, Belding, or Muskegon and considering a short sale, contact Hometown Development. We’ve helped dozens of West Michigan families sell with dignity—and without delay.